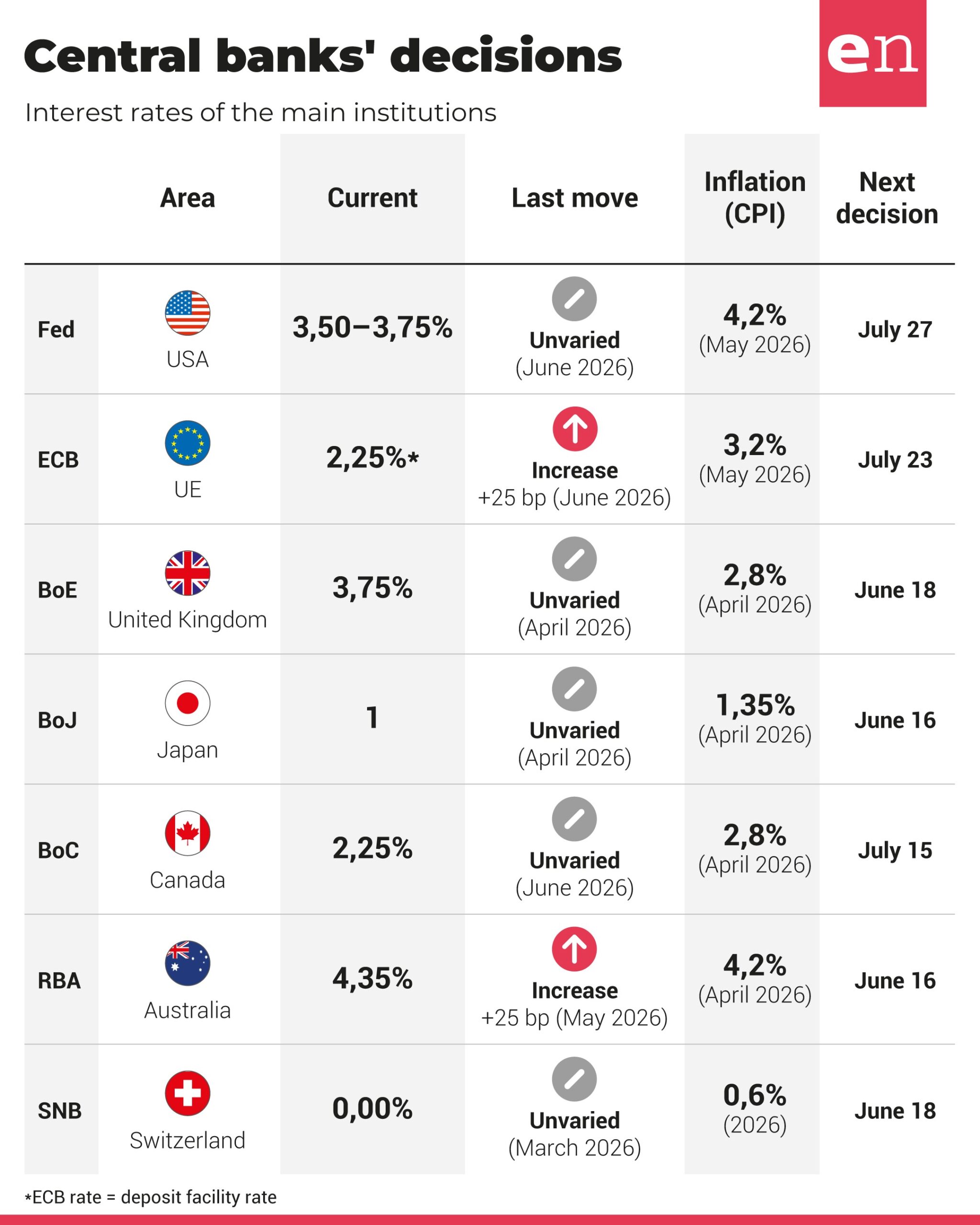

Brussels – Should interest rates be raised further to counter the effects of the war in Iran? The Central Bank cannot rule this out. “We are confident that with an appropriate monetary policy, inflation will return to the target level,” explains ECB President Christine Lagarde during her hearing at the European Parliament on Committee on Economic Affairs. An “open-ended” response, suggesting that the Eurotower is prepared to raise interest rates following the decision already taken should the situation deteriorate and inflation rise further.

However, as Lagarde acknowledges, it is hoped that there will be no need for further tightening of monetary policy. It is true, she reiterates, that “we will follow a data-dependent approach” and decisions will be taken “on a case-by-case basis”; however, “compared with the previous bout of inflation, at this stage the current shock appears to be of a lesser magnitude and is occurring in a different context.”

The war in Iran “is pushing up inflation,” Lagarde points out. In this upward trend, “the main driver of inflation since February has been rising energy inflation,” and the ECB President compares the current situation with the one triggered by the outbreak of the war in Ukraine. In 2022, “the economy was emerging from the pandemic, which had created significant macroeconomic imbalances, including supply chain disruptions and highly accommodative monetary and fiscal policies to support the recovery.” However, she continues, “at the start of the current shock, inflation was closer to the target and monetary and fiscal policy were no longer highly accommodative.” For Lagarde, this suggests that the transmission may be more limited, although risks remain should the shock intensify or persist.”

Inflation falling and growth picking up: ECB data

After all, the estimates available to the Central Bank do not predict anything dire. On the contrary, the Eurotower’s economists, in the data released in June, forecast an overall inflation rate of 3 per cent in 2026, 2.3 per cent in 2027 and 2 per cent in 2028. There is therefore a downward trend, tending towards a return to the 2 per cent reference target. It is here, Lagarde clarifies, that the ECB could opt for further rate rises. Because “if inflation is expected to deviate significantly and persistently from the target, our response will need to be sufficiently forceful or persistent to prevent self-reinforcing dynamics from taking hold and to avert the risk of inflation expectations becoming unanchored.”

However, the ECB President does not wish to fuel fears, and goes so far as to reassure: “At present, we see no evidence of a loss of anchorage in inflation expectations or of second-round effects that would justify a more forceful policy response at this stage.” This means that a further rise in interest rates is not on the cards, at least not in the immediate future, and that if the situation were to remain as it is, a pause might be envisaged.

The underlying problem is the overall situation: “The outlook remains uncertain, with upside risks to inflation and downside risks to economic growth,” states Lagarde, who explains: “The peace agreement in the Middle East is welcome, but the situation remains fragile, with risks of setbacks or further escalation.”

As for growth, the Eurosystem staff projections for June 2026 forecast increases in real gross domestic product of 0.8 per cent in 2026, 1.2 per cent in 2027, and 1.5 per cent in 2028. Lagarde reassures MEPs and the markets: “Aggregate growth of 0.8 per cent across the entire eurozone is not stagnation.”

English version by the Translation Service of Withub

![Il vertice dei leader Ue si apre con tensioni su Schengen. La Germania chiede una soluzione [foto: imagoeconomica]](https://www.eunews.it/wp-content/uploads/2022/12/Imagoeconomica_1366264-scaled.jpg)